There are certain forces in play that will seriously affect the lives of generations coming after us. The current generation is only barely cognizant of the forces that will change the lives of those who will follow us.

Whether we could have changed the outcome will be debated by historians in the future but with the situation as it is currently, it is what it is.

In the U.S. and elsewhere, improvement in healthcare, the increase in birth control devices and the increase in abortions have created a population curve which measured against social and pension costs is unsustainable.

Only in third-world countries that have subsistence living standards does the younger generation have a fighting chance of being able to support the older generations.

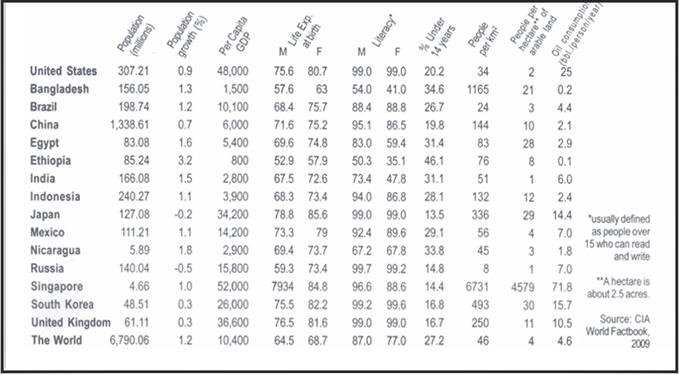

The following table shows some of the disparity between sovereign nations. The population for India is incorrectly stated and should be 1166.08 million. The data shows the wide differences in population growth, per capital GDP, life expectancy, literacy levels and population density among others. These factors will play an important part in how the world evolves during the balance of the 21st century.

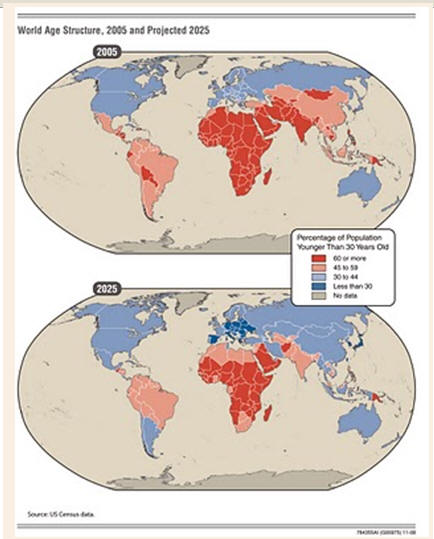

The following chart illustrates the changes in the age structure of countries between 2005 and 2025 showing the percentage of the population that is younger than 30 years old. Clearly shown is the increasing aging of the Chinese and Indian population as well as much of Southeast Asia during this period. This increase could create demand for products and services or if not met the increase could also foment political unrest throughout the region.

History is full of situations where wars were used to control the population growth although that may not have been obvious.

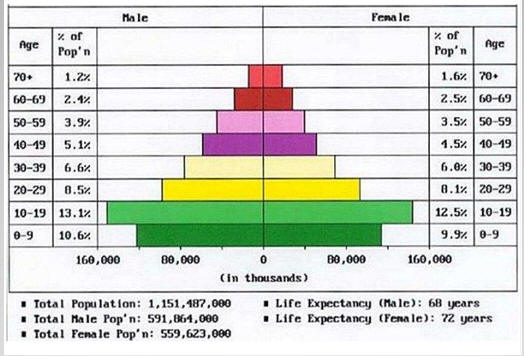

The following aging trees, or aging pyramids, for selected countries shows the wide difference as of 2007 that will shape each countries economic future. Those countries with a wide base of the population tree, relatively high retirement age and low social cost structures like government pensions and health-care costs have a significantly higher chance of surviving a major upheaval to their sovereign nation status in the future.

The United States with their "baby boomer" generation moving quickly toward retirement, a social security program that is quickly headed towards negative levels, a new health-care entitlement program coupled with Medicare and Medicaid soaring cost as well as a huge federal and state debt and future unfunded liability problem is facing serious financial difficulties going forward.

The U.S. with its abortion policies and the increasing use of contraception measures has seen its birth rate decline during the past three decades.

The US 'AAA' debt rating could be in serious jeopardy and the increased cost of interest on the country's debt might have a damaging effect upon future financing options.

The contrast to China's population is striking as shown in the next chart. Note that the percent of the population over the age of 60 is less for China than it is for the U.S. The life expectancy in China for both men and women is less than that in the U.S. The 'one child policy' of China has had an major effect on the population growth but is no coming under fire from the population as males out-number females and competition for brides is becoming most interesting.

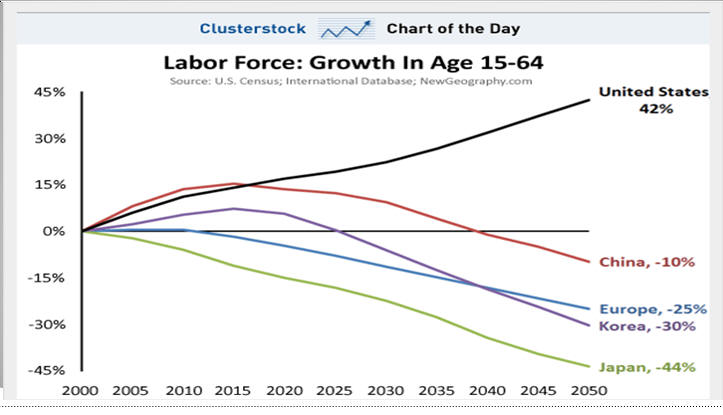

In terms of absolute numbers, there is no comparison between the U.S. and China labor force growth. However, in looking at the growth in the labor force from 2000 to 2050 in the 15-64 age group, the U.S. will grow at a faster rate than most areas as shown below.

For a country to maintain its culture, it is believe by most demographers that a fertility rate of 2.11 is the minimum required. The following chart shows the fertility rates for selected European countries. There are only two solutions to a declining fertility rate ... increasing birth rates and/or immigration.

The United Kingdom has long allowed easy immigration from its Commonwealth countries. However, that has also eroded over time, the British culture into a melting pot that is now in danger of becoming something quite different from the England of the mid-20th century. With the advent of the Euro zone, immigration became even more lax and the result is a country that has an increasing level of friction between the old Christian nation and a growing population of Moslem population demanding Sharia law.

If the much higher birth rates of the Moslem population are not tempered (in France, the Moslem birth rate is 8:1), the entire European continent will become dominated by the Islamic culture by 2050. In 2009, there were more Mosques in France than the total of Christian churches and Jewish synagogues combined.

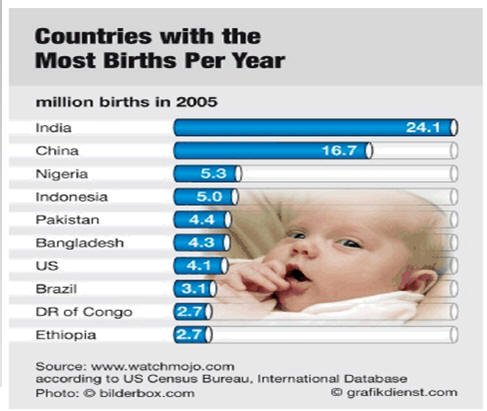

The countries with the highest birth rates tend to be those in the third world. The countries with the absolute largest numbers of births are shown in the following chart and India and China are number 1 and 2. However, Nigeria, Indonesia and Pakistan and Bangladesh are number 3 to 6 and the economic outlook for those children do not appear to be very good.

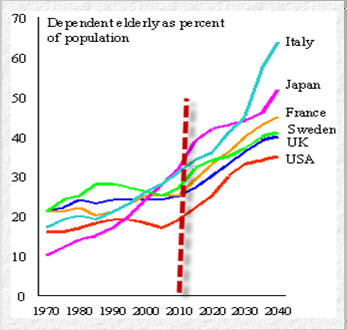

A major problem with the current aging pyramid is that as society ages, the costs associated also increases. The following graph shows that Italy, Japan and France are falling major increases in the percent of their population in the next 30 years while the US is in relatively good shape. Unfortunately, each country will still have to make significant reductions in the level of benefits currently promised to those defined as 'elderly' or face major unfunded liability problems in the years ahead.

Life expectancy is a major component facing those countries with high pension costs. The following chart shows life expectancy for the top 10 countries. Obviously, we should move to Andorra or San Marino.

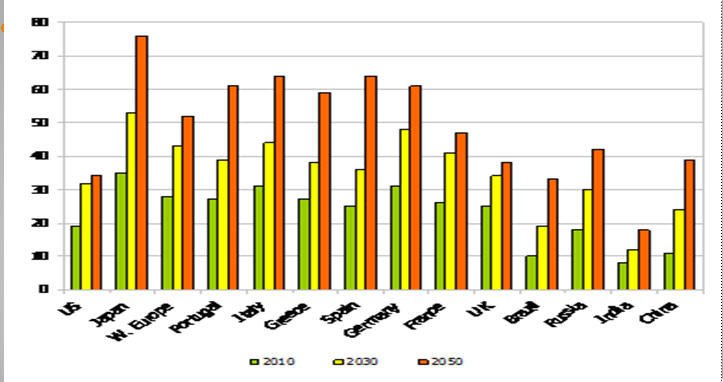

The next chart shows for various countries the percentage of the population that will be over 60. The failure to fund those pension and health-care costs will put a major burden on economic growth going forward.

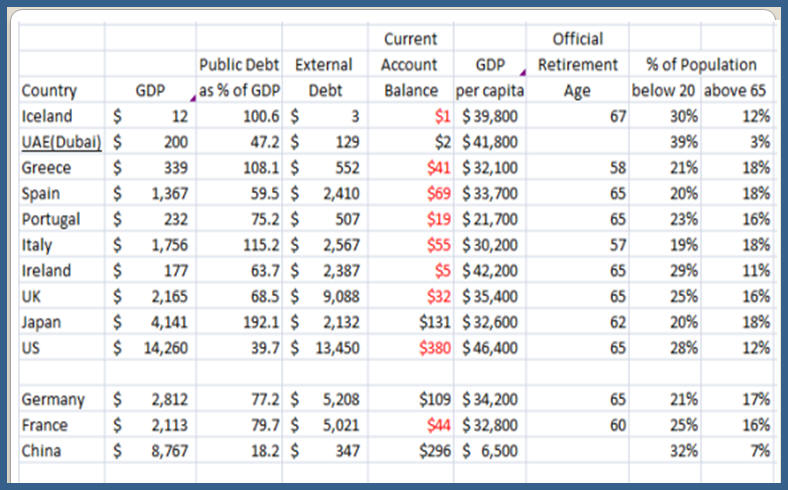

Debt has become the opiate of choice for most sovereign governments. It is the easiest way to provide for expensive programs and to use the power of the purse to remain in power. Over the centuries, governments have used debasement of their currency to remain in power until confidence disappeared. Today's fiat currencies are in danger of continuing that legacy. Whether it was Iceland, Dubai and/or Greece that was the 'canary in the coal-mine' can be argued but the fact is we are in the midst of a competitive world-wide devaluation.

The limit to the ability of a central bank to create money is the acceptability of the underlying bonds and currency.

Whether it is the dollar, Euro, yen and renmimbi, today's currencies are in the process of seeing a fundamental realignment.

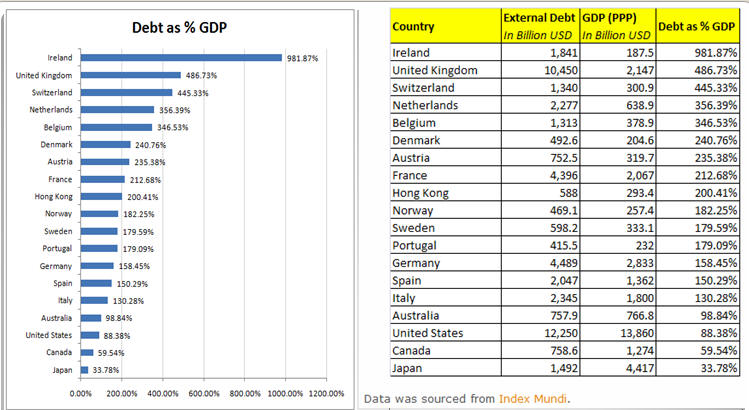

The following chart and table purports to state the relative position of debt/GDP of selected countries as of 12-31-2008. Based upon various recent disclosures about swaps and unfunded liabilities, can any of the data be relied upon?

For example, the so-called debt of the U.S. is stated as being only $12,250 billion whereas at the same time, the Federal Reserve Bank of Dallas had a study that suggested that the stated debt and unfunded liabilities of the U.S. as of the end of 2008, the real number was closer to $1,040,000 billion. Just a slight difference.

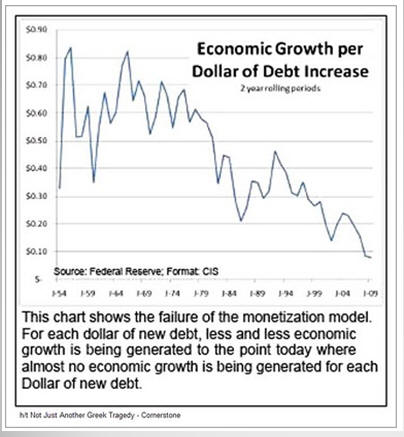

As governments have moved away from the capitalist system espoused by Adam Smith towards a socialist European system style advocated by John Maynard Keynes, the impact of government intervention for a dollar's worth of incremental government debt has declined dramatically. In the U.S., the recent huge stimulus programs have not been seen to be beneficial to economic growth. At best, the trillions of dollars in taxpayer funds have only been useful to prop up 'too big to fail' banks and corporations that should have failed.

The current Euro zone bailout is another example of stimulus funds serving to protect French and German banks from the bad decisions which they previously made. Moreover, the Euro currency as well as the Euro zone zone itself will probably implode because it is a financial and not a political union.

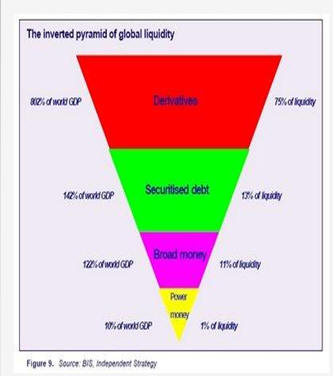

One of the missing 'D's' is derivatives and the growth of those financial instruments threatens the financial stability of most markets. The problem is the concentration, lack of transparency, failure to understand the concepts of counter-party risk and the "mark-to-fantasy' accounting techniques used to value derivatives.

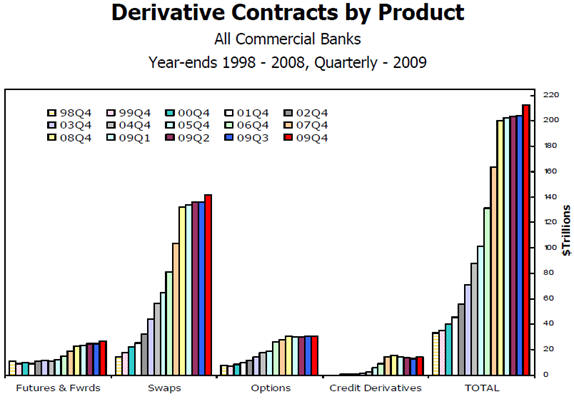

Originally developed as a hedge against uncertainty, the growth of derivatives is now nothing more than speculation with all the elements of a Ponzi scheme. The fact that both parties to a derivatives transaction can value the transaction using different assumptions about risk leads to each party being able to report the trade as profitable. Simply put, elementary accounting suggests that is impossible. Derivatives have simply become speculative gambling on a huge scale and has produced a huge pyramid of inverted wealth as shown in the following chart.

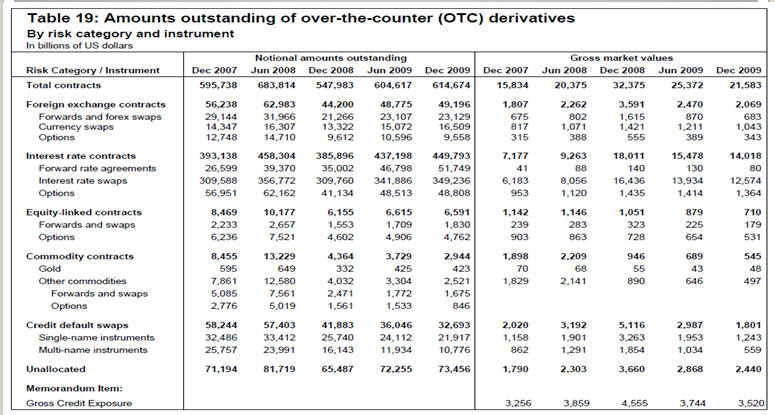

World GDP is about $64 trillion while the notional amount of derivatives outstanding as estimated by the Bank for International Settlements (BIS) is almost 10 times as great, or $614 trillion at the end of 2009. Despite a faltering economy, the notional value of derivatives held by U.S. commercial banks increased $8.5 trillion in the fourth quarter of 2009, or 4.2%, to $212.8 trillion. Moreover, this growth happened during a period of restrained economic growth.

BIS prepared the following data table in their 4th Quarter 2009 report showing the growth of various types of derivatives during the past five years.

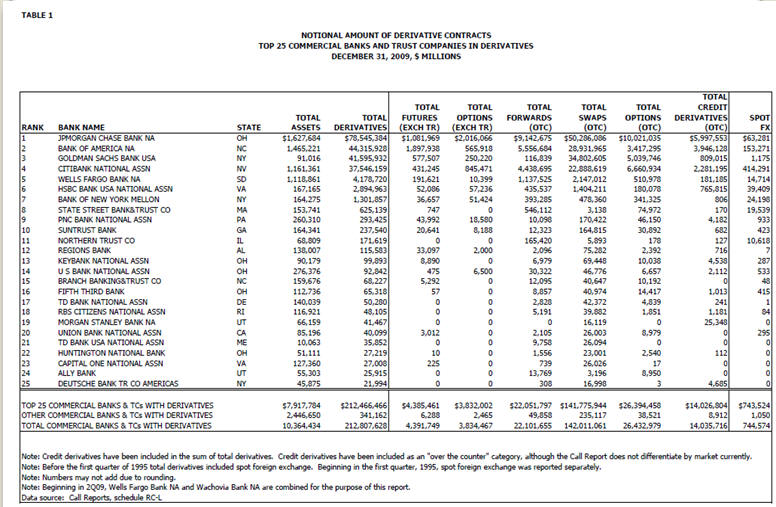

The US Comptroller of the Currency in its 4th Quarter 2009 report had the following chart showing the growth of various derivative products and concentration of derivatives held by US commercial banks. Clearly, the top five banks in the US had the major exposure to derivative risk.

An analysis of the derivative contracts shows that interest rate swaps were the bulk of all contracts. The banks were trying to hedge their exposure to changes in the interest rates. However, the real question arises as to what happens if one of the parties is unable to perform. Will the Federal Reserve once again step in to make everyone whole like they did in the AIG meltdown? Moreover, what is the risk that as alluded to above, what happens to the system if the Federal Reserve is seen as insolvent.

With short-term interest rates at historic lows and the bond spread recently near record levels, the possibility exists that the Federal Reserve could be on shaky ground. It will not be the first time that a central bank has gone under.

How do you go bankrupt? The answer is simply ... suddenly! In a world dominated by fiat currencies, confidence is all that really stands behind a currency. It is not gold, IMF drawing rights, currency swaps nor is it military might. When confidence goes, it is gone and it takes generations to recover.

Iceland, Dubai and Greece have provided recent examples of the swiftness of the swift erosion of confidence and the slide into chaotic conditions.

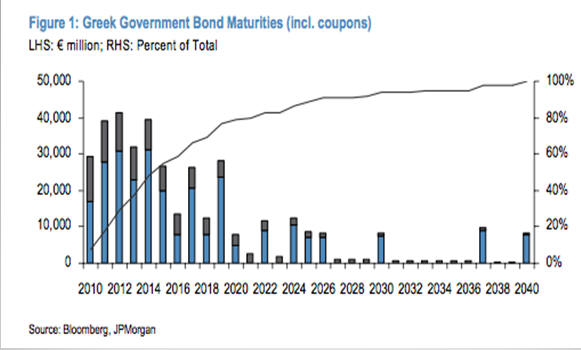

For our purposes, we shall look to Greece in more detail. Greece had a problem with not only its current budget deficit but had allowed its debt maturity schedule to compress into a narrow time frame thus causing a significant funding problem. The following chart shows the maturity schedule.

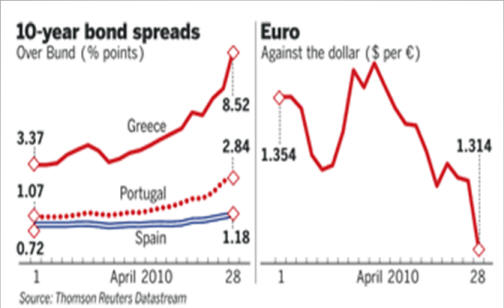

As the magnitude of the refinancing required became apparent as the Greek interest rate swaps with Goldman Sachs were discovered, the bond vigilantes sprung into action and beginning in late 2009 started increasing the bond spreads for Greek bonds dramatically as shown in the following chart. Ireland, unlike Greece, had a similar problem but decided to take measures like controlling public pay raises and reducing costs which so far has seemed to control its problem.

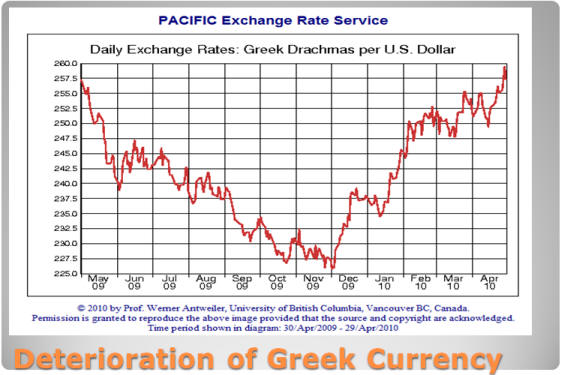

The effect on the value of the Greek currency vs. the U.S. dollar is shown in the following chart. In effect, the bond vigilantes began to run the table on Greece at the beginning of December 2009.

The sudden impact during April 2010 of Greek's demise can be seen dramatically in the following charts as various plans were set forth to handle what in effect was the failure of French and German banks holding Greek government bonds. If those bonds were not rolled over and/or redeemed, major French and German banks still reeling from the effects of the financial meltdown of sub-prime mortgages could collapse.

At the final hour, the German's were forced into playing banker to the European Union along with a deal with the U.S. Treasury and the International Monetary Fund. It remains to be seen if anything has really changed except to borrow some more time.

Adding more debt to an over-leveraged situation only adds to the problem and does not solve it. Will the austerity measures proposed for the Greek government and its population actually occur? What happens if the current bailout package does not solve the problem and/or falls apart?

Will Greece be able to change its culture to abide by the draconian measures demanded by the Euro zone and the IMF? Is it possible to change the cultural differences and the widespread tax evasion and government corruption endemic to Greece?

The proposed $1 trillion bailout, if successful, will only buy time and not solve the problem that exists which is simply too much debt caused by governments living beyond their means.

While Greece and the other PIIGS are the accidents the markets are currently focused upon, the real problem lies somewhere else ... the United Kingdom and the United States.

The following chart using data from the CIA Factbook suggests that perhaps the real problem is being overlooked.

However, Greece does confirm how confidence is lost and bankruptcy appears ... suddenly!

With the demographic problem placing forces in play that can only be overcome with a higher fertility rate and/or the destruction caused by wars, the world is facing unpopular choices. None of the choices allow for a continuation of the status quo and all suggest that economic growth going forward is likely to be constrained.

In certain areas, economic growth may be helped by technological developments but the timing of those is at best uncertain. Innovation is not something that can be forecast or developed on a precise timeline. Moreover, some of the improvements in biomedicine only extend life expectancy thereby adding to the debt load. The development of other technologies, however, can reduce the economic costs. Technology can be a double-edged sword.

Politicians are not willing to make hard choices and eliminate entitlement programs. Increasing taxes to pay for those programs reduces economic growth. Moreover, capital generally moves to where it can maximize its after-tax returns ... a lesson which many politicians will learn going forward.

Hence, we have two bad choices ... two missing 'D's'. Deflation and Disaster ... the only question is when!

But then - 'Tis Only My Opinion!

Fred Richards

May 1, 2010

Corruptisima republica plurimae leges. [The more corrupt a republic, the more laws.] -- Tacitus, Annals III 27

This issue of 'Tis Only My Opinion was

copyrighted by Strategic Investing in 2010.

All rights reserved. Quotation with attribution is encouraged.

'Tis Only My Opinion is intended to provoke thinking, then dialogue among

our readers.

![]()

![]() 'Tis Only My Opinion! Archive Menu

'Tis Only My Opinion! Archive Menu

Last updated - December 20, 2009